Understanding Business Credit Fundamentals

Business credit represents your company's creditworthiness and financial reputation in the commercial marketplace. Unlike personal credit, business credit is tied to your company's Employer Identification Number (EIN) and operates independently of your personal credit score. This separation allows business owners to protect their personal assets while building corporate financial strength.

Business credit scores typically range from 0 to 100, with higher scores indicating better creditworthiness. Major business credit bureaus including Dun & Bradstreet, Experian Business, and Equifax Business maintain these records and provide scores that lenders, suppliers, and partners use to evaluate your company's financial reliability.

The foundation of strong business credit rests on several key factors: payment history, credit utilization, length of credit history, types of credit accounts, and the overall financial health of your business. Each of these elements contributes to your credit profile and influences how financial institutions and trade partners view your company.

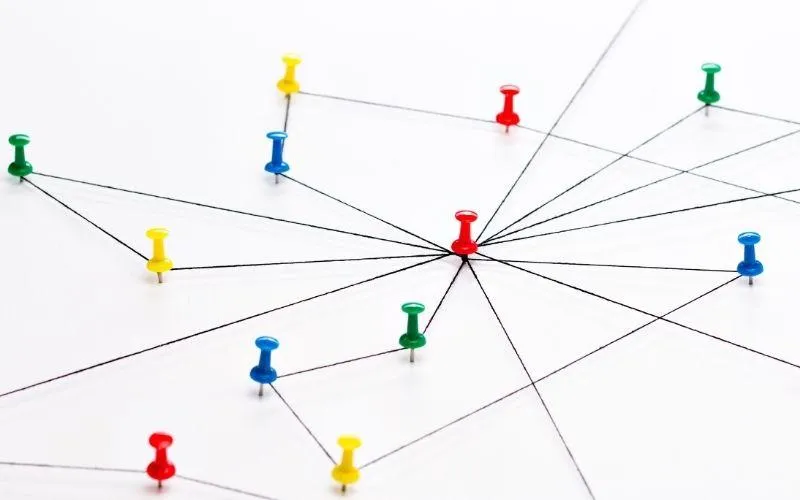

Trade lines represent the individual credit accounts that appear on your business credit report. Each trade line contains detailed information about a specific credit relationship, including the creditor's name, account type, credit limit, current balance, payment history, and account status. These entries serve as the building blocks of your business credit profile.

Trade lines can originate from various sources including banks, credit card companies, equipment financing companies, and importantly for this discussion, suppliers and vendors who extend trade credit. When a supplier reports your payment behavior to business credit bureaus, they create a trade line that reflects your company's payment patterns and reliability.

The quality and diversity of trade lines significantly impact your business credit score. Positive trade lines showing consistent, timely payments boost your creditworthiness, while negative entries reflecting late payments or defaults can severely damage your credit profile. The age of trade lines also matters, as longer-established credit relationships demonstrate stability and experience in managing business obligations.

What Are Trade Lines?

Net Terms Explained

Net terms represent payment agreements between businesses that specify when payment is due after goods or services are delivered. The most common arrangement is Net 30, meaning payment is due within 30 days of the invoice date. Other variations include Net 15, Net 60, and Net 90, with the number indicating the payment window in days.

These payment terms serve multiple purposes in business relationships. For buyers, net terms provide crucial cash flow benefits by allowing time to receive, process, and potentially

resell goods before payment is required. For sellers, offering net terms can be a competitive advantage that attracts customers and builds loyalty, though it also creates accounts

receivable that must be managed carefully.

Net terms essentially function as short-term, interest-free loans from suppliers to their customers. This arrangement allows businesses to leverage their suppliers; financing to fund operations, inventory, and growth initiatives. However, this benefit comes with the responsibility to pay according to agreed terms, as failure to do so can damage business

relationships and credit standing.

The interaction between business credit, trade lines, and net terms creates a powerful system for building creditworthiness while managing cash flow. When you establish net terms with suppliers who report to credit bureaus, each transaction becomes an opportunity to demonstrate financial responsibility and build positive credit history.

This relationship begins when you apply for trade credit with suppliers. They evaluate your business credit score, financial statements, and payment history to determine whether to

extend credit and under what terms. Companies with stronger credit profiles typically qualify for more favorable net terms, higher credit limits, and better pricing.

Once established, your payment behavior on these net terms creates trade lines that appear on your business credit reports. Consistently paying within the agreed timeframe builds positive payment history, while late payments create negative marks that can persist for years. This creates a feedback loop where good credit leads to better terms, and responsible use of those terms further improves credit.

The timing of payments within net terms significantly affects credit building. Paying early or on time consistently demonstrates reliability, while taking the full term allowed shows you can effectively manage cash flow without missing deadlines. Some suppliers even offer early payment discounts, creating opportunities to improve both cash flow and supplier relationships.

The Critical Connection: How These Elements Work Together

Building and Managing Trade Lines Effectively

Establishing your first trade lines requires a strategic approach, especially for new businesses with limited credit history. Start by identifying suppliers in your industry who report payment activity to business credit bureaus. Not all suppliers report to credit agencies, so research or directly ask potential trade partners about their reporting practices.

This system also enables businesses to separate operational cash flow from growth investments. By using supplier credit for routine inventory and operational needs, companies can preserve cash and traditional credit lines for expansion opportunities, equipment purchases, or emergency situations. This strategic allocation of financial resources often proves critical for long-term success.

Building a strong portfolio of positive trade lines through responsible use of net terms also improves your ability to access traditional financing. Banks and lenders view businesses with established trade credit relationships and positive payment histories as lower-risk borrowers, potentially leading to better loan terms, higher credit limits, and more financing options.

The networking aspect of trade relationships cannot be overlooked. Suppliers who extend credit often become invested in their customers success, potentially leading to better pricing, priority treatment during shortages, extended terms during difficult periods, and valuable business referrals.

Understanding and strategically using the interaction between business credit, trade lines, and net terms offers numerous benefits for growing businesses. The most immediate advantage is improved cash flow management. Net terms allow you to receive inventory or services upfront while deferring payment, effectively providing interest-free financing that can be crucial during growth phases or seasonal fluctuations.

This system also enables businesses to separate operational cash flow from growth investments. By using supplier credit for routine inventory and operational needs, companies

can preserve cash and traditional credit lines for expansion opportunities, equipment purchases, or emergency situations. This strategic allocation of financial resources often proves critical for long-term success.

Building a strong portfolio of positive trade lines through responsible use of net terms also

improves your ability to access traditional financing. Banks and lenders view businesses with established trade credit relationships and positive payment histories as lower-risk borrowers, potentially leading to better loan terms, higher credit limits, and more financing options.

The networking aspect of trade relationships cannot be overlooked. Suppliers who extend credit often become invested in their customers' success, potentially leading to better pricing, priority treatment during shortages, extended terms during difficult periods, and valuable business referrals.

Strategic Benefits of Leveraging This System

Common Challenges and How to Overcome Them

One of the most significant challenges businesses face is the "chicken and egg" problem of building initial credit. Suppliers want to see credit history before extending terms, but you need suppliers to create that history. Overcome this by starting with suppliers who specialize in working with newer businesses, providing strong financial documentation, offering deposits or guarantees, and leveraging existing business relationships for referrals.

Cash flow management becomes more complex when dealing with multiple net terms arrangements. Create detailed cash flow projections that account for all payment obligations, and maintain adequate cash reserves to handle unexpected delays in customer payments or seasonal fluctuations. Consider factoring or invoice financing to bridge cash flow gaps when necessary.

Not all suppliers report payment activity to credit bureaus, which means some positive payment behavior may not contribute to credit building. Research suppliers' reporting practices before establishing relationships, and don't hesitate to ask them to begin reporting if they don't currently do so. Some suppliers are willing to start reporting for valued customers.

Managing disputes or quality issues becomes more complex when payment terms are involved. Establish clear communication channels with suppliers and address problems quickly to avoid payment delays that could damage your credit. Document all communications and maintain professional relationships even when resolving difficult situations.

Different industries have varying standard practices regarding net terms and trade credit. Manufacturing and wholesale businesses often operate with longer payment terms due to the nature of their cash conversion cycles, while service businesses might work with shorter terms or immediate payment requirements.

Seasonal businesses face unique challenges in managing trade lines and net terms. Retailers preparing for holiday seasons, construction companies dealing with weather- related fluctuations, or agricultural businesses managing harvest cycles must carefully coordinate their supplier payment obligations with their revenue patterns.

International trade adds complexity to net terms arrangements, with considerations including currency fluctuations, extended shipping times, letters of credit, and different business practices across countries. These factors require more sophisticated cash flow planning and risk management strategies.

Industry-Specific Considerations

Technology and Automation in Trade Credit Management

Modern business management software can significantly improve your ability to manage trade lines and net terms effectively. Accounting systems with integrated accounts payable modules can automate payment scheduling, provide cash flow forecasting, and generate reports that help optimize payment timing.

Electronic data interchange (EDI) systems streamline ordering and invoicing processes with major suppliers, reducing processing time and potential errors that could lead to payment delays. Many suppliers offer early payment discounts for electronic payments, creating additional opportunities for cost savings.

Credit monitoring services provide automated alerts about changes to your business credit reports, new trade lines, and potential identity theft or fraud. These services help ensure you're aware of all credit activity and can respond quickly to any issues.

Supply chain finance platforms are emerging as sophisticated tools that connect buyers, suppliers, and financial institutions to optimize payment terms and cash flow for all parties. These platforms can provide early payment options, extended terms, and financing solutions that benefit entire supply chains.

Once your business has established a solid foundation of trade lines and proven payment history, more advanced strategies become available. Consider negotiating improved terms with existing suppliers based on your payment history and growing relationship. Many suppliers are willing to extend terms, increase credit limits, or provide better pricing for reliable customers.

Supply chain financing programs offered by major suppliers can provide additional flexibility and cost savings. These programs often involve third-party financing companies that pay suppliers immediately while extending terms to buyers, creating benefits for all parties involved.

Some businesses develop strategic relationships with key suppliers that go beyond simple buyer-seller arrangements. These partnerships might include exclusive distribution rights, co-marketing opportunities, or collaborative product development, all built on the foundation of strong credit relationships and reliable payments.

Consider the strategic timing of payments to optimize cash flow throughout the month or quarter. Spreading payment obligations across different dates can smooth cash flow fluctuations and reduce the risk of temporary cash shortages affecting your ability to meet obligations.

Advanced Strategies for Established Businesses

Future Trends and Considerations

The business credit and trade finance landscape continues to evolve with technological advancement and changing business practices. Artificial intelligence and machine learning are being incorporated into credit scoring models, potentially providing more nuanced and accurate assessments of business creditworthiness.

Alternative data sources, including social media activity, online reviews, and digital transaction histories, are beginning to influence business credit decisions. This trend may provide opportunities for businesses with limited traditional credit history but strong operational metrics.

Blockchain technology and smart contracts may eventually automate many aspects of trade credit relationships, from contract execution to payment processing and credit reporting. These developments could reduce costs, improve accuracy, and speed up many current processes.

The increasing focus on supply chain transparency and sustainability may influence trade credit decisions, with suppliers and buyers considering environmental and social factors alongside financial metrics when establishing credit relationships.

The interaction between business credit, trade lines, and net terms creates a powerful ecosystem for building financial strength while managing cash flow effectively. Understanding these relationships and using them strategically can provide significant competitive advantages for businesses of all sizes.

Success in this area requires consistent attention to payment obligations, proactive relationship management with suppliers, and regular monitoring of credit reports and scores. The effort invested in building strong trade credit relationships pays dividends through improved cash flow, better supplier relationships, enhanced access to traditional financing, and increased financial flexibility.

As your business grows and evolves, continue to view trade credit as a strategic tool rather than simply a payment convenience. The foundation you build through responsible management of trade lines and net terms will serve your business well through various economic conditions and growth phases.

The key to maximizing these benefits lies in treating every supplier relationship as an opportunity to demonstrate financial responsibility and build long-term value. By maintaining this perspective and implementing the strategies outlined in this guide, you can create a robust financial foundation that supports sustainable business growth and success.

Want to learn how to build a strong credit profile across all three bureaus?

Book your FREE business credit consultation today.

Leave a Comment

Comments:

©2025 Laughlin Business Credit Advisor, all rights reserved. No reproduction or use of any portion of the content or work, or the entire work, is permitted without the express written permission and authorization of the publisher. However, the publisher of these materials routinely grants authorization for reproduction or use of this work, in whole or in part. If you would like to use any portion of this material in a book, article, e-zine, newsletter, radio or television broadcast, podcast, or in any other seminar, teleconference, or other events or publications, please email or call Laughlin Business Credit Advisor.

Stay inspired, informed, and ahead – fill out the form to join us now!

Dive into our library and unlock a treasure trove of business insights that can transform your journey to success.

Laughlin Business Credit Advisors

680 W. Nye Ln, Ste #201Carson City, NV 89703

All Rights Reserved,

© 2024 Great Basin Holdings, Inc.